1. Introduction

ndia produces nearly 350 million tonnes of agricultural waste per year (Naidu, 1999). It has been estimated that 110-150 million tonnes crop residues is surplus to its present utilization as a cattle feed, constructional and industrial raw material and as industrial fuel. Due to their heterogeneous nature, biomass material possesses inherently low bulk densities and thus it is difficult to efficiently handle large quantities of most feedstock. Therefore, large expenses are incurred during material handling, transportation, storage etc. Transportation had the 2nd highest cost by considering all factors, when the biomass power plant was run at full capacity (Kumar et al.2003). It is noted that transportation cost will increase with increasing power plant size. In order to combat the negative handling aspects of bulk biomass, densification is often required. If such crop residues are converted into briquettes they can provide huge and reliable source of feedstock for thermo chemical conversion (Anonymous, 2002). Apart from the problems of transportation, storage and handling, the direct burning of loose biomass in conventional grates is associated with very low thermal efficiency and widespread air pollution (Grover and Mishra, 1996). In India total area under cashew nut cultivation 7,20,000 ha of which 76,270 ha are productive producing 4,50,000 MT of cashew. On an average shell makes 50 % of weight of nut while CNSL makes 15 to 30 per cent of shell production of cashew nut shells may be estimated to 2,25,000 MT from available statistics (Raina & Kulkarni, 2005). The CNSL removed, deoiled shells are abundantly available as a biomass waste. The waste biomass generated in cashew processing is utilized as a substitute to wood fuel or thrown as waste. This biomass requires much energy to make it in powder form for briquette. On such typical task, only the solution is to convert this biomass firstly into activated carbon form which is easier to make briquette from carbonization of cashew nut shell, grass, rice husk and hence keeping in view study is undertaken.

2. II.

3. Materials and Methods

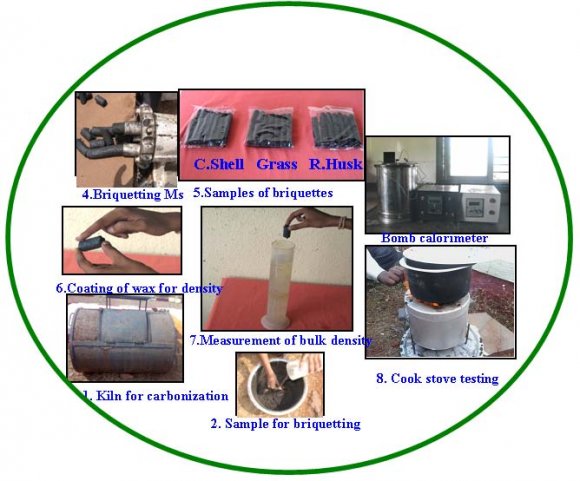

The carbonized biomass samples were obtained by burning them in a kiln. A kiln made up of a cylindrical metal drum which incommoded about 100 kg of biomass. A kiln was closed with metal lid after loading with biomass as shown in Fig 1 (1). Little amount of biomass was used in the firing portion to ignite the kiln. Due to absence of air heat spreaded over a biomass and carbonized samples were obtained.

4. a) Process for briquette preparation

The carbonized cashew shell, rice husk and grass were used as major constituents for briquetting without any binding material. The various combinations of major constituents were tried in order to get briquettes of the desired quality. Different combinations as 50:25:25, 25:50:25 and 25:25:50 for cashew shell, rice husk and grass were made for observing the properties of briquettes. The known quantity of water was added in mixture using thumb rule for that the material should get bind by hand pressing after addition of water. The mixture was fed to briquetting machine and briquetting machine was operated at rated speed and power. The complete setup for briquettes preparation and testing is shown in The screw press extruder type briquetting machine was used in the present study. It consists of driving motor, screw, die, and hopper and power transmission system. Pulley and belt were used to transmit power from motor to the screw. The raw material was fed to the hoppers, which convey it to screw by gravity. The material was pushed forward due to geometry of screw. As the material was pushed, it got compressed and binded material comes out of die in the form of briquettes. The detail technical specification of screw extruder type briquetting machine is shown in Table 1.

5. Economic Analysis

The cost analysis was carried out as complete briquettes processing of cashew shell, rice husk, saw dust, glyricidia and cow dung, grass residue briquettes by screw press technologies, in order to compare the three types of combinations briquettes in respect of their economics.

Following economic indicators were used for economic analysis of briquettes prepared from caebonized cashew nut shell and other selected biomass under this study. The present values of the future returns calculated through the use of discounting. Discounting was essentially a technique by which future benefits and cost streams can be reduced to their present worth. The process of finding the present worth of a future value is called discounting. The discounting rate is the interest rate assumed for discounting.

6. Global Journal of Researches in Engineering

An agricultural project returns the same benefit for several years and we need to know the present worth of that future income stream to know how much it was justified in investing today to receive that income stream. After deducting capital investment from gross benefit what is left over is a residual that is available to recover the investment made in the project. The residual is the net benefit stream.

The most straightforward discounted cash flow measure of project worth is the net present worth (NPW). The net present worth may be computed by subtracting the total discounted present worth of the cost stream from that of the benefit stream. Another way of using the incremental net benefit stream or incremental cash flow for measuring the worth of a project is to find the discount rate that makes the net present worth of the incremental net benefit stream or incremental cash flow equal to zero. This discount rate is called the internal rate of return. It is the maximum interest that a project could pay for the resources used if the project is to recover its investment and operating costs and still break even. It is the rate of return on capital outstanding per period while it is invested in the project. The internal rate of return is a very useful measure of project worth. This ratio was obtained when the present worth of the benefit stream was divided by the present worth of the cost stream. The formal selection criterion for the benefit-cost ratio for measure of project worth was to accept projects for a benefit-cost ratio of 1 or greater.

In practice, it was probably more common not to compute the benefit-cost ratio using gross cost and gross benefit, but rather to compare the present worth of the net benefit with the present worth of the investment cost plus the operation and maintenance cost. The ratio will be computed by taking the present worth of the gross benefit less associated cost and then comparing it with the present worth of the project cost. The associated cost is the value of goods and services over and above those included in project costs needed to make the immediate products or services of the project available for use or sale. Project economic cost is the sum of installation costs, operation and maintenance cost and replacement costs. The payback period is the length of time from the beginning of the project until the net value of the incremental production stream reaches the total amount of the capital investment. It shows the length of time between cumulative net cash outflow recovered in the form of yearly net cash inflows.

7. IV.

8. Results and Discussions

Cost analysis was carried out to check economic acceptability of briquetting plant by considering following assumptions: 1. Proportion of carbonized material to raw material is 1:3.3 i.e. is 30% of raw material. 2. Cost of briquetted fuel was 7 Rs/kg. 3. Output of machine was 36 kg/hr, 41 kg/hr, and 22.5 kg/hr for cashew shell, grass and rice husk respectively. 4. Initial cost of fabrication of machine was Rs. 10000. 5. Total electricity used during operation of plant was 2 kwh/day. 6. Total days for plant operation was 300 days. 7. Cost of electricity unit was 5 Rs. 9 that the cost of the plant is recovered within 8 months only i.e. the pay back period of the plant was only 0.68 and 0.63 years for cashew shell and grass briquetted fuel respectively and after that the unit will produce net profit. Whereas payback period of rice husk briquetting plant is 29.35 months i.e. 2.5 years.

9. Cost of installation for different briquetted fuel is depicted in

10. V.

11. Conclusions

It was observed that combination of grass briquetted fuel is more economical than other combinations. It has net present value of Rs. 2256434.38, pay back period of 7.56 month and benefit cost ratio was 2.93.

| Sr. no. | Particular | Specifications | |

| 1 | Screw dimensions | No of turns | = 4 |

| Screw pitch | = 6 cm | ||

| Maximum diameter of screw | = 9 cm | ||

| Minimum diameter of screw | = 6 cm | ||

| 2 | Die dimensions | No of exit tubes | = 3 |

| Diameter of exit tube | = 2.5 | ||

| cm | |||

| Length of exit tube | = 4 cm | ||

| 3 | Voltmeter | Analog with range | = 0 to |

| 300V | |||

| 4 | Ammeter | Analog with range | = 0 to 30 |

| A | |||

| 5 | Pulley and belt | Diameter of driven pulley | = 26 cm |

| Diameter of driving pulley | = 9 cm | ||

| Belt type | V-belt | ||

| 6 | Motor | Single phase induction motor | |

| Power | = 1Hp | ||

| Speed | = 1425 | ||

| rpm | |||

| 7 | Overall dimensions | Overall length of machine | = 31 cm |

| Overall width of machine | = 31 cm | ||

| Overall height of machine | = 62 cm | ||

| III. |

| Year 2013 |

| XIII Issue v v v I Version I |

| Volume |

| D D D D ) C |

| ( |

| Global Journal of Researches in Engineering |

| Sr. No. | Item | Quantity | Rate | Cost (Rs.) |

| 1 | Cost of casing + cost of | 1 | 10000 | 10000 |

| motor | Rs. | |||

| 2 | Labour | 300 days | 150 Rs. | 45000 |

| 3 | Raw material | 178200 kg | 0.5 | 89100 |

| (36 kg/hr) | Rs./kg | |||

| Total | 144100 |

| Sr. No. | Item | Quantity | Rate | Cost (Rs.) |

| 1 | Cost of casing +cost of motor | 1 | 10000 Rs. | 10000 |

| 2 | Labour | 300 days | 150 Rs. | 45000 |

| 3 | Raw material | 202950 kg (41 kg/hr) | 0.5 Rs./kg | 101475 |

| Total | 156475 |

| Sr. No. | Item | Quantity | Rate | Cost (Rs.) |

| 1 | Cost of casing +cost of motor | 1 | 10000 Rs. | 10000 |

| 2 | Labour | 300 days | 150 Rs. | 45000 |

| 3 | Raw material | 111375 kg (22.5kg/hr) | 1 Rs./kg | 111375 |

| Total | 166375 |

| Sr. No. | Particulars | Cashew shell | Grass | Rice husk |

| 1 | Briquettes (kg) | 54000 | 61500 | 33750 |

| 2 | Total revenue from | 378000 | 430500 | 236250 |

| briquetted fuel (Rs.) | ||||

| 3 | Cost of briquette | 89100+45000 | 101475+4 | 111375+4 |

| preparation (Binder, | = 134100 | 5000=146 | 5000 | |

| water, chemicals, labour | 475 | =156375 | ||

| etc) (Rs.) | ||||

| 4 | Initial investment of | 10000 | 10000 | 10000 |

| (Rs.) | ||||

| 5 | Cost of electricity (Rs.) | 3000 | 3000 | 3000 |

| 6 | Total operation and | 500 | 500 | 500 |

| maintenance cost (Rs.) |

| Year 2013 | ||||||

| I | ||||||

| XIII Issue v v I Version | ||||||

| Volume | ||||||

| D D D D ) C | ||||||

| ( | ||||||

| Global Journal of Researches in Engineering | Year (1) 0.0 1.0 2.0 3.0 | Cash outflow (2) 147100.0 137100.0 137100.0 137100.0 | PW of Cash outflow (3) 147100.0 123513.5 111273.4 100246.3 | Cash inflow (4) 0.0 378000.0 378000.0 378000.0 | PW of Cash inflow (5) 0.0 340540.5 306793.3 276390.3 | NPW (5)-(3) -147100.0 217027.0 195519.8 176144.0 |

| 4.0 | 137100.0 | 90312.0 | 378000.0 | 249000.3 | 158688.3 | |

| 5.0 | 137100.0 | 81362.2 | 378000.0 | 224324.6 | 142962.4 | |

| 6.0 | 137100.0 | 73299.3 | 378000.0 | 202094.2 | 128795.0 | |

| 7.0 | 137100.0 | 66035.4 | 378000.0 | 182066.9 | 116031.5 | |

| 8.0 | 137100.0 | 59491.3 | 378000.0 | 164024.2 | 104532.9 | |

| 9.0 | 137100.0 | 53595.8 | 378000.0 | 147769.6 | 94173.8 | |

| 10.0 | 137100.0 | 48284.5 | 378000.0 | 133125.7 | 84841.2 | |

| 11.0 | 137100.0 | 43499.5 | 378000.0 | 119933.1 | 76433.6 | |

| 12.0 | 137100.0 | 39188.8 | 378000.0 | 108047.8 | 68859.1 |

| Year 2013 | |||||

| Volume | |||||

| D D D D ) | |||||

| ( | |||||

| Year | Cash outflow | PW of Cash outflow | Cash inflow | PW of Cash inflow | NPW |

| Particulars | Cashew shell | Grass | Rice husk |

| Net Present Worth | 1935370.8 | 2256434.3 | 631948.8 |

| (Rs) | |||

| Pay Back Period | 0.68 | 0.63 | 2.5 |

| (Years) | (8.1 months) | (7.56 months) | (29.35 |

| months) | |||

| Internal Rate of | 374.0 | 428.0 | 230.0 |

| Return (%) | |||

| BCR for first year | 2.8 | 2.93 | 1.51 |